In an increasingly unpredictable world, global mobility is becoming an important part of how investors, entrepreneurs and internationally minded families think about long-term security. The question is no longer limited to where someone lives today, but how much flexibility they have if personal, political, economic, regulatory or financial circumstances change in the future.

A well-structured Plan B is not built on fear. It is built on preparation, diversification and the ability to make decisions before urgency limits the available options. For some families, this may mean securing a reliable residence base in another country. For others, it may involve second citizenship, a stronger passport, a real estate-linked residency route, or a broader structure that separates lifestyle, mobility and asset planning across more than one jurisdiction.

At Citiverse, we view Plan B planning as part of a wider global mobility strategy. The objective is not simply to obtain a residence permit or a second passport. The objective is to create a practical framework for freedom, continuity and long-term optionality. The right structure depends on the applicant’s nationality, family profile, investment objectives, lifestyle preferences, tax position and future plans. There is no universal Plan B. A serious strategy should be tailored, compliant and built around the specific outcomes the client wants to secure.

Global mobility has become a serious strategic consideration for investors and families who want to reduce dependency on a single country, passport, banking system or regulatory environment. Political changes, tax reforms, banking restrictions, currency instability, tightening visa rules and regional uncertainty can all affect how individuals live, travel, invest and operate internationally. These changes do not always happen gradually. In many cases, the families best positioned to respond are those that already have alternative residence or citizenship options in place.

This is why passport diversification has become a growing topic among globally minded investors and families. However, a complete Plan B goes beyond the passport itself. A second passport can be valuable, but it is only one layer of a broader international strategy. A well-designed Plan B may include an alternative country of residence, a second citizenship, access to a stronger or more suitable passport, a reliable relocation route, family security, investment optionality, succession planning and potential tax residency considerations. The strongest plans are built before they are needed, when the applicant has time to compare jurisdictions, prepare documentation properly and choose the route that fits their long-term objectives.

In global mobility planning, a Plan B is a practical framework for preserving choice. It is not simply about obtaining a document or selecting the fastest available program. It is about creating a second layer of access, security and flexibility that can be used if personal or external circumstances change.

Depending on the client’s profile, a Plan B may include a residence permit, permanent residency, citizenship by investment, a real estate-backed relocation option, or a coordinated structure across several jurisdictions. For some applicants, residence may be enough. For others, citizenship may be the stronger long-term solution. In more complex cases, residence and citizenship should be combined with banking, asset holding or business structuring considerations. The key question is not “Which program is best?” The more useful question is: “What should this Plan B achieve?”

For one family, the priority may be a European base. For another, it may be broader travel freedom. For an entrepreneur, it may be access to a jurisdiction that supports business continuity and international banking. For a family office, it may be multi-generational security, succession planning and jurisdictional diversification. A serious Plan B should be built around purpose, not noise.

A strong Plan B is rarely based on one document or one jurisdiction. In many cases, the most effective approach is a layered strategy, where residence, citizenship and asset positioning each serve a different purpose.

This is where global mobility planning becomes more than a passport discussion. A family may choose one jurisdiction as a lifestyle and residence base, another for citizenship and travel flexibility, and a third for asset holding, banking, succession or investment structuring. The objective is not complexity for its own sake. The objective is to reduce dependency on one country and create usable options across several areas of life. A practical structure may look like this.

Cyprus Permanent Residency by Investment may provide a stable Mediterranean base, access to an EU environment, real estate-linked planning and a long-term relocation option for families seeking lifestyle, continuity and security.

Caribbean Citizenship by Investment may support broader travel flexibility, second nationality planning and reduced reliance on a single passport. For some investors, this layer is particularly relevant where mobility, banking access or international travel flexibility are central objectives.

A third jurisdiction may be considered for holding assets, managing investment structures, establishing business presence or improving banking optionality, depending on the client’s legal, tax and family profile. This layer should always be reviewed with qualified legal and tax advisors, because asset structuring must be aligned with residence, citizenship, tax residency and long-term succession objectives.

This type of structure is not about collecting passports or residence permits. It is about assigning a clear function to each jurisdiction. One country may serve as the place to live. Another may provide citizenship and travel flexibility. A third may support asset protection, banking or international business planning.

When coordinated properly, these layers can create a stronger and more resilient international position than relying on one country for every aspect of personal, family and financial life.

One of the most common mistakes in global mobility planning is treating residence and citizenship as if they provide the same result. They do not.

Residency generally gives the right to live in a country, subject to the specific rules of the program. It may support relocation, regional access, lifestyle planning, education planning, tax residency planning or a long-term presence in a chosen jurisdiction. Citizenship provides nationality. In many cases, it may also provide access to a passport, consular protection and a more permanent legal relationship with the country granting citizenship.

For a detailed comparison, Citiverse has prepared a dedicated guide on Residency by Investment vs Citizenship by Investment.

In the context of Plan B planning, the distinction matters. A family seeking a reliable European residence base may not need immediate citizenship. A business owner seeking wider travel flexibility may place greater value on a second passport. A client planning for future relocation may prefer a residence route that aligns with property ownership, lifestyle and long-term presence. Neither option is automatically better. The right choice depends on the intended outcome.

For many successful individuals and families, financial diversification is already part of normal planning. Assets may be held in different currencies, investment portfolios may span several markets, and business interests may operate internationally. Yet personal legal status is often still concentrated in one place: one passport, one residence base, one banking environment and one set of domestic rules.

That concentration can create exposure. If travel access changes, banking becomes more difficult, tax rules shift, political conditions become less predictable, or relocation suddenly becomes necessary, a family without alternative residence or citizenship options may have limited room to manoeuvre.

Jurisdiction diversification addresses this risk by separating different needs across different places. One country may be suitable as a lifestyle base. Another may be more relevant for citizenship and international mobility. A third may be considered for asset holding, business structuring or wealth planning. The purpose is not to disconnect from one country completely. The purpose is to avoid relying on only one country for every important aspect of personal, family and financial life.

A strong global mobility plan should begin with a structured assessment. Before selecting a program, applicants should understand their objectives, constraints and risk profile. The most suitable route will depend on several practical factors.

Family structure

Family eligibility rules differ significantly between programs. Some routes allow a spouse and dependent children to be included. Others may also permit parents, grandparents or other qualifying dependants. Age limits, dependency rules and documentation requirements vary by jurisdiction. A Plan B should be designed around the whole family, not only the main applicant. This is particularly important where the objective includes children’s education, future relocation, family succession or long-term security for dependants.

Current nationality and passport strength

The value of second residence or second citizenship depends partly on the applicant’s current nationality. A person with strong existing travel access may be focused more on relocation, lifestyle or tax positioning. A person with a more restrictive passport may place greater importance on mobility, visa-free access and alternative travel documentation. This is why the same program can have different value for different applicants. The right analysis should begin with the applicant’s current passport, travel needs and long-term objectives.

Residence objectives

Some clients want a place to live immediately. Others want a future relocation option. Some want a European base, while others prefer a flexible residency route that does not require full relocation. For clients exploring residence-led planning, Residency by Investment Programs can provide a structured route to residence rights through qualifying investment.

Citizenship objectives

For applicants seeking nationality, long-term optionality and a second passport, Citizenship by Investment Programs may be more relevant. Citizenship by investment should be assessed carefully. Processing timelines, due diligence requirements, family eligibility, investment routes and long-term benefits differ from one jurisdiction to another. A second citizenship should be selected for strategic fit, not simply because it appears fast, popular or cost-efficient.

Investment structure

Some programs are donation-based. Others are linked to real estate, funds, business investment or other qualifying assets. The investment route should fit the applicant’s financial profile, liquidity preferences, risk appetite and long-term planning objectives. A lower headline cost is not always the best value. Applicants should consider total cost, government fees, due diligence fees, professional fees, family member costs, holding periods, resale conditions and maintenance obligations.

Tax position

Global mobility planning should not be reviewed in isolation from tax considerations. Residence rights, citizenship, time spent in a country, business activity, personal income, asset ownership and family relocation can all have tax implications.

A second residence or citizenship does not automatically change tax residency. Tax residency is usually determined by physical presence rules, domestic legislation, centre of vital interests, treaty provisions and other factual circumstances. A Plan B should therefore be coordinated with qualified tax and legal advisors where relevant. The objective is not only to obtain status. The objective is to create a structure that works in practice.

Timing and certainty

The best time to build a Plan B is before it becomes urgent. Many residence and citizenship routes require document collection, due diligence, source-of-funds review, government processing and investment execution. Waiting until circumstances change can reduce the range of available options. Prepared applicants have more control, more choice and more time to build a compliant application.

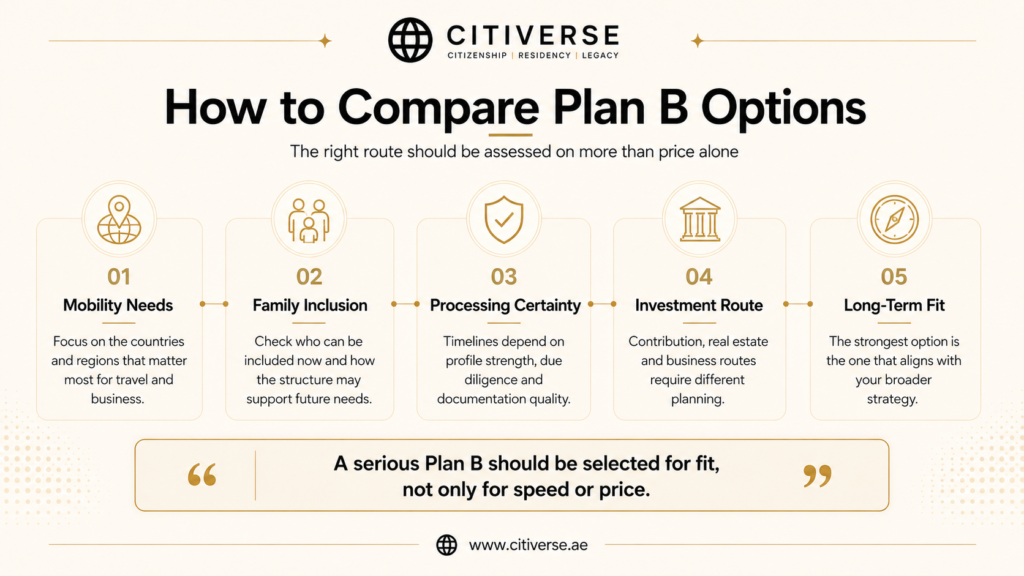

Before selecting a residence or citizenship program, applicants should look beyond headline cost and processing speed. These factors matter, but they should not be the only decision criteria. A serious Plan B should be assessed through several layers:

This framework is important because the cheapest option is not always the right option, and the fastest option is not always the most strategic. A Plan B should be selected for fit, not only for speed or price.

Residency by investment can be suitable for applicants who want a defined legal base in another country without necessarily seeking immediate citizenship. This may be particularly relevant for families seeking lifestyle flexibility, access to a stable jurisdiction, property ownership, regional mobility or a future relocation route.

For example, Cyprus Permanent Residency by Investment may appeal to investors looking for a European residence option linked to real estate. Cyprus can be especially relevant for applicants who value location, lifestyle, business access and a long-term family base in the Eastern Mediterranean. Residency by investment is often less about obtaining a passport and more about creating a reliable place to go. For many families, that is already a powerful layer of security.

Read more about Cyprus Permanent Residency by Investment in 2026: A Real Estate Guide for International Investors

Citizenship by investment may be suitable for applicants who want direct access to second citizenship, subject to the legal requirements and due diligence standards of the relevant jurisdiction. For many internationally active individuals, second citizenship can support broader mobility, reduce reliance on a single nationality and create long-term optionality for the family.

Certain regions remain particularly relevant for citizenship planning. For example, Caribbean Citizenship by Investment continues to attract applicants who are looking for established second citizenship routes, family inclusion options and a practical path to an additional nationality.

However, citizenship by investment should never be selected only because it appears popular, fast or inexpensive. The right program should match the applicant’s objectives, nationality, family structure, documentation profile, investment preference and long-term strategy.

Read more about Caribbean Citizenship by Investment: How to Choose the Right Program